Founded in 1996 in Connecticut, Booking Holdings (BKNG) is the world’s largest online travel company by a huge margin, beating its competitors in size and scale. The company started as Priceline.com and in 2005 the company acquired Booking.com for $133 million. From there, the company keep acquiring other companies such as Agoda.com and Kayak.com

Currently, the company is the biggest online travel company in the world, surpassing Airbnb. Through its company and all of its subsidiaries, Booking Holdings provides travel services to 220 countries in the world.

*revenue figures are for FY25

Booking Holdings started as a hotel-focused OTA, but today it offers:

- Hotels & alternative accommodations

- Flights

- Car rentals

- Attractions/activities

- Restaurant reservations (OpenTable)

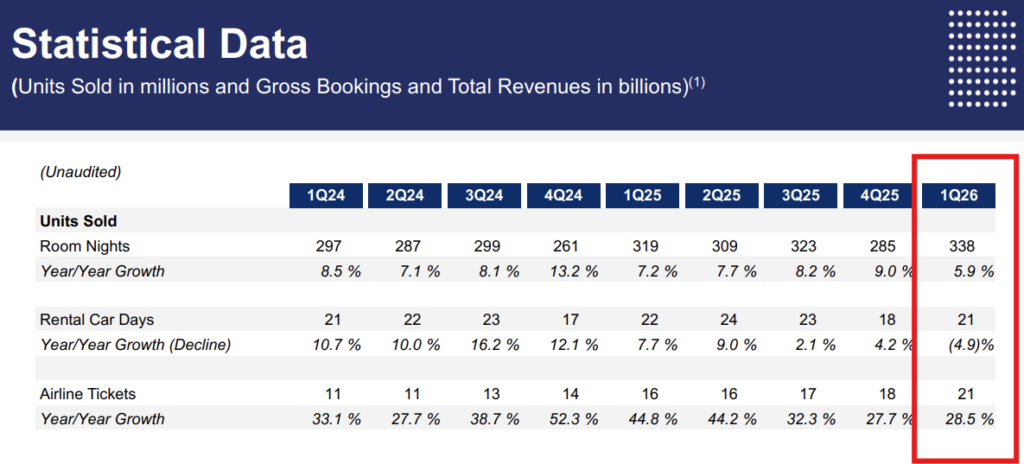

However, from the 1Q26 Report we can find that the majority of the unit sales are from room bookings, not flights or car rentals.

The company does not disclose revenue by sector; however, in previous SEC filings, it stated that 89% of revenue comes from accommodation services. So, while flights have grown handsomely over the years, as shown in the figure above, hotels remain the core business by a wide margin.

What’s interesting is that flight bookings have been one of BKNG’s fastest-growing areas recently. Management has been pushing a “Connected Trip” strategy:

Book the flight → hotel → rental car → attractions all within the Booking ecosystem.

For the business model itself, OTA typically charges 15-20% on gross bookings. So, let’s say a hotel costs Rp2,000,000; the company does not record this as revenue; it will record Rp 150,000-200,000 as the revenue. In 2025:

- Gross bookings were roughly over $180B.

- Revenue was about $27B.

That implies an overall take rate (revenue ÷ gross bookings) around 14–15%.

That’s one of the key metrics investors watch because it reflects the platform’s pricing power and mix. A stable or rising take rate usually indicates the OTA’s competitive position remains strong.

For BKNG, the ability to consistently collect roughly mid-teens percentages on a massive global booking volume is a big reason the business generates such strong cash flow.

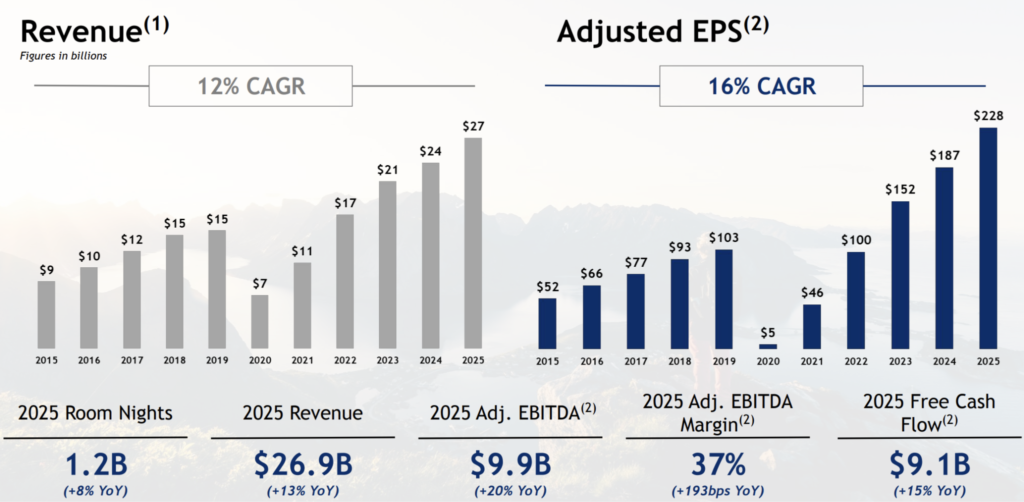

We see that the CAGR for the past 10 years for the revenue is around 12% while for EPS is higher at 16%, indicating stronger pricing power. Since 2015, the revenue has tripled and the net income has quadrupled. In 2020, there was a huge drop in revenue because of COVID-19. A risk for the company would be if there is another pandemic that will slow down global travel. However, it is very unlikely in the next decade or so we have another huge pandemic in the next few years. The Duke Health Institute estimated that the annual likelihood of a pandemic occurring is estimated to be between 2% and 3%, yielding a 47% to 57% probability of another global outbreak in the next 25 years.

This analysis is just getting started. Want the full breakdown? Unlock the complete guide and long-term insights exclusively on our Member Page. Join Supercuan Saham Luar now!